How to Use the Debt to Income Ratio Calculator: Master Your Financial Health in Minutes

Understanding where you stand financially is one of the most important steps toward building wealth and achieving big goals like buying a home or qualifying for better loan rates. One of the key metrics lenders and financial experts look at is your Debt-to-Income (DTI) Ratio. Our free, easy-to-use DTI calculator helps you check your financial health instantly.

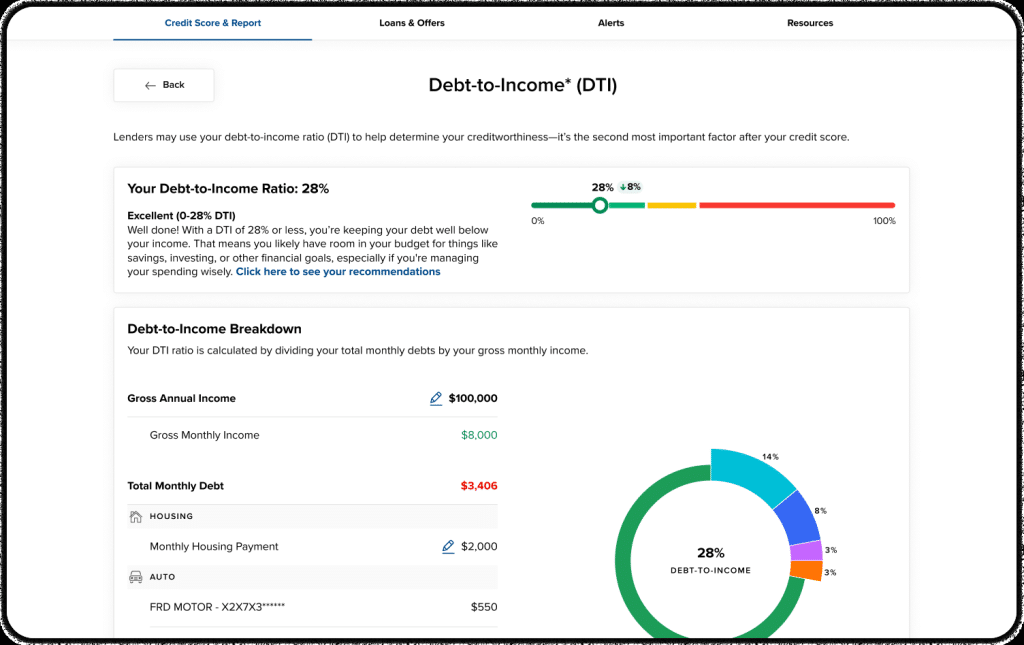

What Is a Debt-to-Income Ratio, and Why Does It Matter?

Your DTI ratio compares your total monthly debt payments to your gross monthly income. It is expressed as a percentage and tells lenders how much of your income is already committed to debts.

Two main types:

- Front-end DTI — Focuses only on housing costs (rent/mortgage, taxes, insurance).

- Back-end DTI — Includes all debts (credit cards, car loans, student loans, etc.).

Lenders generally prefer a back-end DTI under 36%. Anything above 43% can make it harder to get approved for mortgages or other loans.

Step-by-Step Guide: How to Use the DTI Calculator

Step 1: Enter Your Gross Monthly Income Input your total monthly earnings before taxes and deductions. This is the foundation of the calculation.

Step 2: Add Your Monthly Debt Payments Click “+ Add Debt” to list recurring obligations such as the following:

- Mortgage or rent

- Car loans

- Credit card minimum payments

- Student loans

- Personal loans

You can add as many as needed and remove any entry easily.

Step 3: Choose DTI Type Toggle between Front-end (housing only) and Back-end (all debts) depending on your goal.

Step 4: Click “Calculate DTI.” The tool instantly shows your ratio with a clear health status:

- Excellent (≤20%)

- Good (≤36%)

- Fair (≤43%)

- High Risk (>43%)

You’ll also see recommendations tailored to your results.

Real-World Examples

Example 1: Homebuyer Scenario Monthly income: $6,000 Housing payment: $1,800 Other debts: $550 → Back-end DTI ≈ 39% → “”Fair”—Consider paying down credit cards before applying for a mortgage.

Example 2: Strong Financial Position Monthly income: $8,000 Total debts: $1,800 → DTI = 22.5% → “Excellent” — Great position for new financing or investment opportunities.

Pro Tips for Improving Your DTI

- Pay down high-interest debts aggressively.

- Increase your income through side gigs or raises.

- Avoid new debt before major purchases.

- Refinance existing loans for lower payments.

- Track your progress monthly using the calculator.

Understanding the Bigger Picture: DTI vs Credit Score

While DTI measures your current cash flow, your credit score reflects your payment history. Both matter for loan approvals.

Common Questions (FAQs)

What income should I use? Use gross monthly income (before taxes).

Does the calculator include taxes or insurance? Add them manually if they are part of your debt payments.

How often should I check my DTI? Monthly or before any major financial decision.

Is this calculator accurate for loan applications? It gives a reliable estimate. Lenders may use slightly different calculations.

Conclusion: Take Control of Your Finances Today

Knowing your debt-to-income ratio is a powerful first step toward better financial decisions. Our DTI calculator makes it fast, accurate, and completely free.

Try the Debt to Income Ratio Calculator now and see where you stand. Share your results in the comments or reach out if you need help interpreting them.

Start building a stronger financial future today.