📈 Certificate of Deposit (CD) Calculator

Advanced returns projection: compound interest, monthly contributions, tax & inflation adjustment — full visibility, no cutoff

In today’s uncertain economy, smart savers are turning to Certificates of Deposit (CDs) for safe, predictable growth. But calculating returns manually? That’s tedious. Enter the tool.CD Calculator — a free, user-friendly online tool designed specifically to calculate returns on certificates of deposit instantly and accurately.

Whether you’re a beginner saver or an experienced investor comparing multiple CD options, this calculator removes the guesswork. In this complete guide, we’ll walk you through everything: what CDs are and how to use the tool. The CD calculator includes its key benefits, the pros and cons of CD investing, real-world examples, and pro tips to maximize your money.

What Is a Certificate of Deposit (CD)?

A Certificate of Deposit (CD) is a low-risk savings product offered by banks and credit unions. You deposit a lump sum for a fixed term (3 months to 5+ years) and earn a guaranteed interest rate—usually higher than a regular savings account. Your money is FDIC-insured up to $250,000, making it one of the safest places to park cash.

The catch? Early withdrawal usually triggers a penalty, so CDs reward patience. That’s why accurate return projections matter—and that’s exactly what the tool does. CD Calculator delivers.

How the tool works. CD Calculator Works

The calculator uses the industry-standard compound interest formula:

Maturity Value = P × (1 + r/n)^(n×t)

Where:

- P = Principal (initial deposit)

- r = Annual interest rate (as decimal)

- n = Number of times interest compounds per year

- t = Time in years

It instantly shows:

- Total amount at maturity

- Interest earned

- Effective annual yield

- Optional yearly breakdown and comparison charts

No spreadsheets. No math headaches. Just results.

How to Use the Tool. CD Calculator: Step-by-Step Guide

Using the tool is incredibly simple — even if you’ve never calculated interest before.

- Enter your initial deposit type and the amount you plan to invest (minimum usually $500–$1,000 depending on the bank).

- Choose the Term Length Select from common CD terms: 3 months, 6 months, 1 year, 18 months, 2 years, 3 years, 4 years, or 5 years. (Custom months/years supported.)

- Input the APY or Interest Rate Most banks advertise APY (Annual Percentage Yield), which already accounts for coPlease enter it here to ensureit here for the most accurate results.

- Select Compounding Frequency (optional): Choose Monthly, Quarterly, Daily, or Annually. Many CDs compound daily or monthly.

- Click “Calculate Returns.” In under a second, you’ll see:

- Final balance

- Total interest earned

- Breakdown by year (if term > 12 months)

- Visual growth chart

Pro tip: Run multiple scenarios side-by-side to compare banks or terms.

Benefits of Using the Tool. CD Calculator

- Instant & Accurate: No more manual spreadsheets or guessing.

- Scenario Comparison: Test different deposits, rates, and terms in seconds.

- Financial Planning: See exactly how much you’ll have for a house down payment, vacation, or retirement.

- Free & Private: No sign-up, no ads, no data collection.

- Educational: Learn how compounding frequency and term length dramatically affect returns.

- Mobile-Friendly: Works perfectly on phones, tablets, or desktops.

Users report saving hours of research time and making more confident decisions.

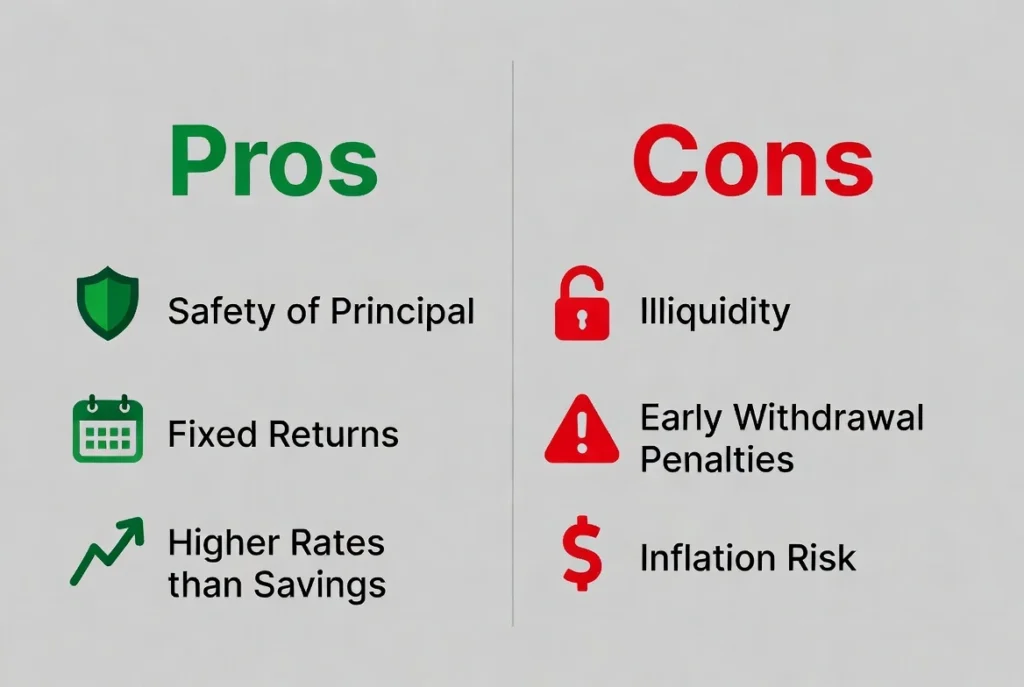

Pros and Cons of Certificates of Deposit

Pros of CDs

- Safety First: FDIC or NCUA insured — your principal is protected.

- Predictable Returns: A fixed rate means you know exactly what you’ll earn.

- Higher Rates than Savings Accounts: Often 2–4x more than regular savings.

- No Market Risk: Unlike stocks or crypto, your money doesn’t fluctuate.

- Discipline Builder: Forces you to leave money untouched.

Cons of CDs

- Early Withdrawal Penalties: Lose months of interest (or principal in rare cases).

- Illiquidity: Money is locked until maturity.

- Opportunity Cost: If rates rise later, you’re stuck; stocks may outperform long-term.

- Inflation Risk: If inflation exceeds your APY, your purchasing power shrinks.

- Minimum Deposits: Some banks require $1,000+ to open.

Bottom line: CDs are ideal for conservative savers who don’t need immediate access to funds.

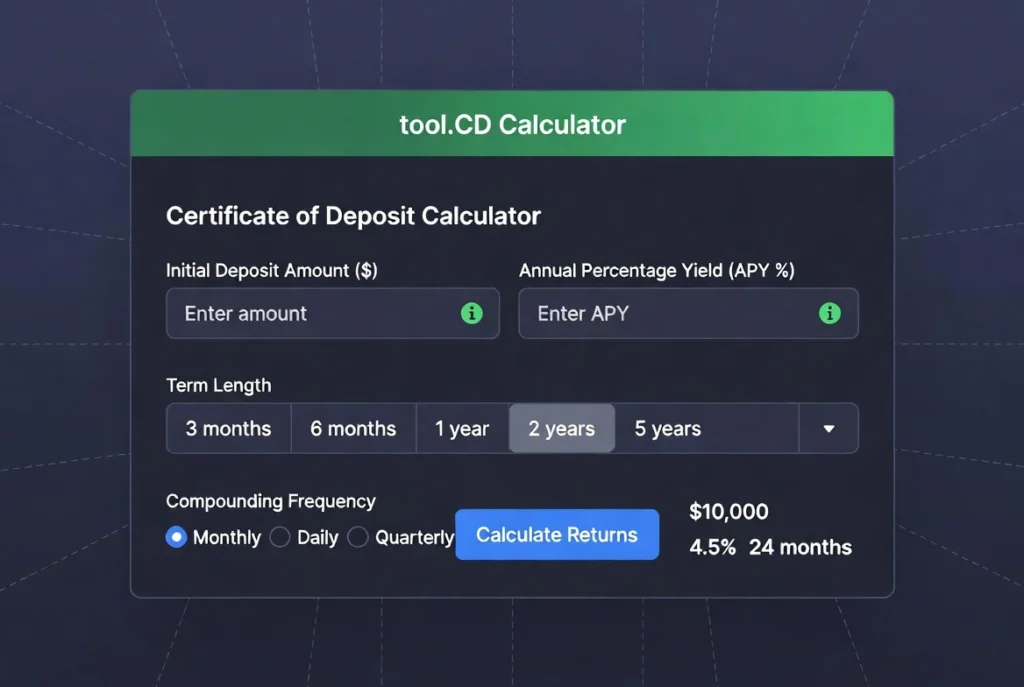

Real-World Example Calculation

Let’s run a sample through the tool.CD Calculator:

- Initial Deposit: $10,000

- APY: 4.5%

- Term: 2 years (24 months)

- Compounding: Monthly

Results:

- Maturity Value: $10,941.68

- Interest Earned: $941.68

- Average monthly interest: ~$39

Try it yourself — change the numbers and watch the chart update live!

Tips to Maximize Your CD Returns in 2026

- Shop around: Online banks and credit unions often offer the best rates.

- Consider CD ladders: Spread money across multiple terms for liquidity and rate flexibility.

- Watch for promotional “no-penalty” CDs.

- Use the calculator to compare against high-yield savings accounts or Treasuries.

- Reinvest at maturity during high-rate environments.

Ready to Grow Your Money with Certainty?

The tool.CD Calculator takes the complexity out of certificate of deposit planning and puts powerful insights at your fingertips.

✅ Try it now — completely free, no registration required. ✅ Compare rates from multiple banks. ✅ Make smarter, data-driven savings decisions today.

Link to the tool.CD Calculator: Use the tool here (replace with your actual URL)

Have questions or want a custom feature added? Drop a comment below — the creator is always improving the tool based on user feedback.

Happy saving! Your future self will thank you for the compound growth.